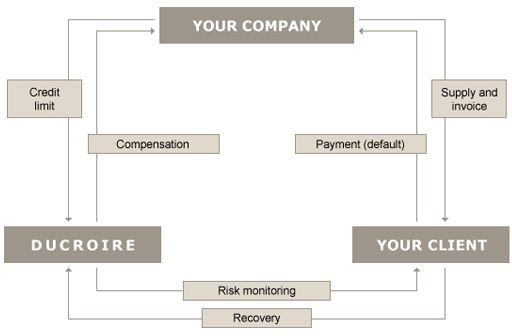

Credit Insurance offers 4 key benefits:

- Risk prevention, enables the Luxembourg company to develop business relations with financially sound customers.

- Regular monitoring of insured customers provides you with information on their payment behaviour, enabling you too better protect yourself against unpleasant surprises.

- Recovery of insured payments by a network of local correspondents

- Compensation for losses on claims in case of your customer’s payment default.

Cover is provided for the risk of non-payment by a customer located abroad, regardless of whether the causes of loss are political, acts of force majeure or commercial events related to the insolvency or default of customers.

ODL can cover both the risk arising before the delivery of goods and service, known as risk of cancellation, and the risk arising after the delivery of goods and services, known as risk of non-payment.

Special Cash Transactions refer to commercial or industrial transactions that due to their nature and complexity require a particular approach. This includes particularly construction works or engineering contracts which take place over several months and are paid as the work progresses.

Fulfilling a contract involves the exporter placing order and incurring expenses. If the buyer cancels the contract, the exporter cannot be sure of recovering the expenses already incurred (risk of cancellation). These expenses may be subject to compensation. In addition to the risk of cancellation, the exporter faces the risk, that the buyer is unable or unwilling to pay once the contract has been fulfilled. The exporter may be compensated for due and unpaid amounts (risk of non-payment).

Cover is provided for the risk of non-payment by the buyers, whether the causes of loss are political, acts of force majeure or commercial relating to the insolvency or default of the customer.

In addition, ODL covers the risk of calling of bank guarantees issued in favor of the buyer, when this call is caused by debtor default under the contract or by a political event.

ODL covers buyer credits granted by banks to foreign buyers to finance exports of contracting equipment, services or construction works, as well as supplier credits arranged by exporters for their foreign contractors for export of contracting equipment and services.

Credits insured by ODL are subject to the rules of the OECD Arrangement on Officially Supported Export Credits.

Buyer Credit Insurance

For buyer credits the bank grants credit directly to the foreign buyer at the exporter’s request. The exporter can draw on this credit to receive cash payment for exports or services provided under the commercial contract.

As credit provider the bank generally wishes to cover itself against the risk of the foreign buyer’s non-reimbursement of the loan.

In this case ODL can cover the bank when the foreign buyer does not repay, partially or late, the buyer credit (principal and interest) for political reasons (risk of currency shortage or transfer difficulties, wars, revolutions etc.), acts of force majeure or commercial reasons related to the insolvency or default of customers.

This cover can also be applied to other forms of medium- and long-term credit relating to export transactions, such as:

- Interbank loans (the foreign bank is the borrower of the loan)

- Project financing (credit granted to a « Special Purpose Company », which is to be repaid primarily from the revenues generated by the project)

- Soft financing (credit granted on concessional terms)

- Financial Leasing.

Through its bank the exporter can offer a fixed rate to its customer thanks to the intervention of ODL via the interest rate stabilisation instrument (1).

Supplier Credit Insurance

A supplier credit is a payment term granted by the exporter to its customer which is generally used in exports of capital goods and services with a value below EUR 5 million and with a granted credit term of less than five years.

ODL insurance protects the exporter against the risk of non-payment by the customer, for political reasons (risk of currency shortage or transfer difficulties, wars, revolutions etc.), acts of force majeure or commercial reasons related to the insolvency or default of customers.

The insurance also offers exporters protection against the risk of cancellation of the export contract for political reasons (risk of currency shortage or transfer difficulties, wars, revolutions etc.), acts of force majeure or commercial reasons related to the insolvency or default of customers.

The exporter may also be insured against the risk of a calling on bank guarantees set up in favor of the buyer, when this call is caused by debtor default under the contract or by a political event.

An exporter wishing to be paid earlier may transfer to its banker the financing of the credit term granted for its customer to their bank . This credit often takes the form of bills of exchange. The bank will be able to pay the exporter by discounting these bills of exchange. This refinancing can take the form of a discount with or without recourse against the exporter. Where this refinancing is granted by the bank without recourse, the bank can insure itself against the risk of non-payment. Where this refinancing is granted by the bank with recourse, the benefit of the exporter may be transferred to the bank.

This cover can also be applied to other forms of medium and long-term credit linked to export operations, such as operational leasing.

(1 ) An important advantage of buyer credit cover is that the exporter, through the intervention of the bank, is able to offer credit at a fixed rate thanks to the intervention of the ODL. This means that the customer knows in advance the financial burden that will fall on him for the duration of the loan.

The OECD Arrangement determines the minimum fixed rate (CIRRs, Commercial Interest References Rates) that can be offered. CIRRs are published monthly.

The ODL’s intervention is based on the difference between the guaranteed fixed rate (Commercial Interest Reference Rate or CIRR) and the interest rate at which banks refinance themselves on the short-term market, plus a bank commission.

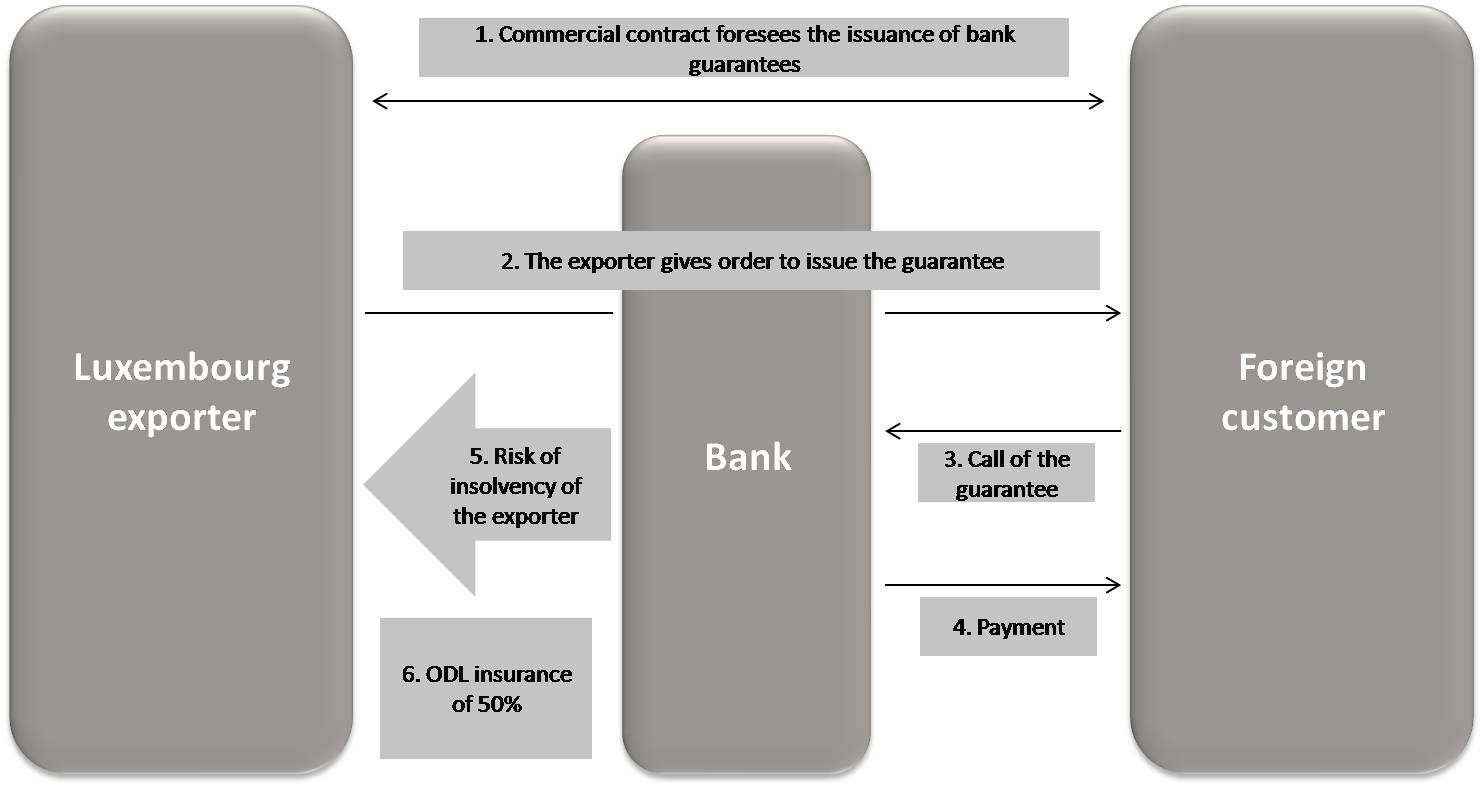

The Office du Ducroire may cover the bank guarantees the exporter has to arrange in favour of the buyer in order to guarantee his contractual obligations. In some cases, the beneficiaries under such guarantees can claim against them “on first demand” without having any proof of the exporter’s fault.

The Ducroire’s insurance of contract guarantees protects the exporter against both unfair calling of the bonds and calling due to a political event or decision.

Guarantees that fall within the scope of the cover are bid bonds, advance payment bonds, performance bonds, etc.

The exporter may be required to emit a bid bond when participating in a tender or public procurement, in order to assure the buyer against a possible withdraw of his contract offer or refusal to sign the contract once it has been awarded.

The advance payment bond enables the buyer to recover the down payment made to the exporter in case the contract should not, or only partly, be performed.

The performance bond is emitted in order to guarantee the buyer that the contract will be performed within the agreed timeframe and according to the terms of the contract.

The insurance of contractual guarantees is generally provided under a single and common policy together with the basic insurance for the export contract. For the insurance of bid bonds, however, a separate policy is drawn up.